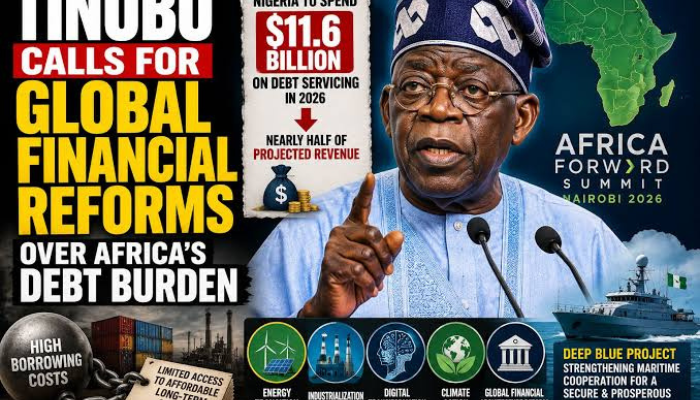

Nigeria will spend approximately $11.6 billion servicing its debt in 2026, representing nearly half of the country’s projected government revenue, President Bola Tinubu has revealed.

Speaking at the Africa Forward Summit in Nairobi on Tuesday, Tinubu called for a fundamental overhaul of the global financial architecture, warning that punitive borrowing costs are draining resources that should be flowing into industry, infrastructure, and small business growth.

Read also: Power, skills, and finance gaps keep Nigerian SMEs stuck in survival mode

The debt burden in plain terms

Nigeria’s debt servicing bill has more than doubled in a single year, rising from $5.15 billion in 2025 to a projected $11.6 billion in 2026 according to data from the Debt Management Office. Tinubu framed the scale of the cost in direct terms at the summit, co-hosted by Kenyan President William Ruto and French President Emmanuel Macron and attended by leaders from more than 30 countries.

Every dollar leaving the treasury to service punitive interest rates is a dollar that does not go into steel, textile mills, agro-processing plants, or digital industries, Tinubu said — and it is a dollar that does not train engineers or provide affordable power for factories.

Read also: Bumpa, Vendorcredit launch Bumpa Capital to expand credit access for Nigerian SMEs

Why this matters for Nigerian businesses

For SMEs and the broader private sector, the consequences of a government stretched thin by debt obligations are practical and immediate. When public revenue is consumed by debt repayment, the fiscal space available for business environment improvements, infrastructure investment, energy subsidies, and direct SME support programmes shrinks accordingly.

Tinubu acknowledged that Nigeria has undertaken painful domestic reforms, including petrol subsidy removal, exchange rate unification, banking recapitalisation, and exit from the Financial Action Task Force grey list. Those reforms have delivered a debt-to-GDP ratio projected at 32.3 per cent in 2026 and lifted external reserves to $45.5 billion. Yet he argued that the gains are being steadily eroded by a global system that continues to treat African sovereigns as permanently high-risk borrowers regardless of fiscal performance.

An industrial base being starved of long-term, affordable capital cannot grow at the pace required to absorb Nigeria’s workforce, support its SMEs, and reduce its dependence on raw material exports.

Read also: Factoring gains ground as alternative funding option for cash-strapped Nigerian SMEs

What the government is pushing for

Nigeria’s position at the summit was not one of seeking aid. Tinubu was explicit that Africa’s economies need a fair financial system that enables industrialisation, supports local manufacturing, and stops rewarding raw material exports while penalising the processing and manufacturing activities that create real economic value.

For small businesses, the message signals continued government pressure on international institutions to create conditions under which domestic investment, SME financing, and industrial development become more viable — even if the structural change needed will take time to materialise.